Not All Interest Is Deductible for Taxes

A frequent question that arises when borrowing money is whether or not the interest will be tax deductible. That can be a complicated question, and unfortunately not all interest an individual pays is deductible. The rules for deducting interest vary, depending on whether the loan proceeds are used for personal, investment, or business activities. Interest expense can fall into any of the following categories:

Personal interest – is not deductible. Typically this includes interest from personal credit card debt, personal car loan interest, home appliance purchases, etc.

Investment interest – this is interest paid on debt incurred to purchase investments such as land, stocks, mutual funds, etc. However, interest on debt to acquire or carry tax-free investments is not deductible at all. The annual investment interest deduction is limited to “net investment income,” which is the total taxable investment income reduced by investment expenses (other than expenses related to investments that produce non-taxable income). The investment interest deduction is only allowed to taxpayers who itemize their deductions.

Home mortgage interest – includes the interest on debt to purchase, construct or substantially improve a taxpayer’s principal home or second home. This type of loan is referred to as acquisition debt. For the interest to be deductible the debt must be secured by the home purchased, constructed, or substantially improved. A secured debt is one in which the taxpayer signs a mortgage, deed of trust, or land contract that makes their ownership in a qualified home security for payment of the debt; provides, in case of default, that the home could satisfy the debt; and is recorded under any state or local law that applies. In other words, if the taxpayer can't pay the debt, their home can then serve as payment to the lender to satisfy the debt.

For Debt Incurred Before 12/16/2017 - the debt for which the interest is deductible is limited to $1,000,000 ($500,000 for married separate).

For Debt Incurred After 12/15/2017 - the debt for which the interest is deductible is limited to $750,000 ($375,000 for married separate).

Passive activity interest – includes interest on debt that's for business or income-producing activities in which the taxpayer doesn’t “materially participate” and is generally deductible only if income from passive activities exceeds expenses from those activities. The most common passive activities are probably real estate rentals. For rental real estate activities, there is a special passive loss allowance of up to $25,000 for taxpayers who are active but not necessarily material participants in the rental. The $25,000 phases out for taxpayers with adjusted gross income between $100,000 and $150,000.

Trade or business interest – includes interest on debts that are for activities in which a taxpayer materially participates. This type of interest can generally be deducted in full as a business expense.

Because of the variety of limits imposed on interest deductions, the IRS provides special rules to allocate interest expense among the categories. These “tracing rules,” as they are called, are generally based on the use of the loan proceeds. Thus interest expense on a debt is allocated in the same manner as the allocation of the debt to which the interest expense relates. Debt is allocated by tracing disbursements of the debt proceeds to specific expenditures, i.e., “follow the money.”

These tracing rules, combined with the restrictions associated with the various categories of interest, can create some unexpected results. Here are some examples:

Example 1: A taxpayer takes out a loan secured by his rental property and uses the proceeds to refinance the rental loan and buy a car for personal use. The taxpayer must allocate interest expense on the loan between rental interest and personal interest for the purchase of the car, and even though the loan is secured by the business property, the personal loan interest portion is not deductible.

Example 2: The taxpayer borrows $50,000 secured by his home to be used in his consulting business. He deposits the $50,000 into a checking account he only uses for his business. Since he can trace the use of the funds to his business, he can deduct the interest as a business expense.

Example 3: The taxpayer owns a rental property free and clear and wants to purchase a home to use as his personal residence. He obtains a loan on the rental to purchase the home. Under the tracing rules, the taxpayer must trace the use of the funds to their use, and as the debt was not used to acquire the rental, the interest on the loan cannot be deducted as rental interest. The funds can be traced to the purchase of the taxpayer’s home. However, for interest to be deductible as home mortgage interest, the debt must be secured by the home, which it is not. Result: the interest is not deductible anywhere.

As you can see, it is very important to plan your financing moves carefully, especially when equity in one asset is being used to acquire another. Please contact your tax advisor for assistance in applying the various interest limitations and tracing rules to ensure you don’t inadvertently get some unexpected results.

Even if You’re Not Required to File a Tax Return, You May Be Missing Out if You Don’t!

Some people may choose not to file a tax return because they didn't earn enough money to be required to file, but these folks may miss out on getting a refund if they don’t file. Although there are some exceptions, generally individuals are not required to file a tax return if their income for the year is below the filing threshold for their filing status as shown in the following table.

Many social benefits provided by the government for lower income individuals are distributed through the tax return, often in the form of a tax credit, and a return must be filed to claim those benefits, many of which can be substantial. Some of these credits are partially or fully refundable even if an individual has no tax liability. So, even though you might not be required to file a return you may be missing out on a tax refund if you don’t file one. Here are some examples:

Withholding – If you are not required to file a tax return but had income taxes withheld from your W-2 wages, Social Security benefits, retirement income, or investment income, or you made estimated tax payments, you are entitled to have that withholding or estimated payments refunded. However, you must file a tax return to recover the withholding or tax payments.

2021 Recovery Rebate Credit – Individuals who didn't qualify for a third Economic Impact Payment or got less than the full amount, may be eligible to claim the 2021 recovery rebate credit . However, a 2021 return will need to be filed, even if not otherwise required to file a tax return. The credit will reduce any tax owed for 2021 or be included in the tax refund.

Earned Income Tax Credit (EITC) - A working individual who earned $57,414 or less in 2021 can receive the EITC as a tax refund. For 2021 the amount of the earned income credit ranges from $1,502 to $6,728 depending on your filing status and how many, if any, children you claim on your tax return. Those who did not file a return for tax year 2020 or 2021 or who did not claim the earned income tax credit on their 2020 or 2021 return because they had no earned income in those years may file an original or amended return to claim the credit using their 2019 earned income if they are otherwise eligible to do so.

Child Tax Credit Or Credit For Other Dependents – individuals can claim the child tax credit for 2021 if they have a qualifying child under the age of 18 and meet other qualifications. Other taxpayers may be eligible for the credit for other dependents. This includes people who have:

Dependents who are age 18 or older.

Dependents who have individual taxpayer identification numbers instead of a Social Security number.

Dependent parents or other qualifying relatives whom the taxpayer supports.

Dependents living with the taxpayer who aren't related to the taxpayer.

Education Credits – There are two higher education credits that can reduce the amount of tax someone owes on their tax return. One is the American opportunity tax credit and the other is the lifetime learning credit. The taxpayer, their spouse or their dependent must have been a student enrolled at least half time for one academic period and have paid college or university education expenses to qualify. The taxpayer may qualify for one of these credits even if they don't owe any taxes.

If you are not required to file, and didn’t, you can contact your local tax office to determine if any benefit can be gained by filing a 2021 tax return. Even if you are required to file and didn’t, they may be able to help you meet your filing requirements and take advantage of the many benefits available!

What Is a Required Minimum Distribution?

Required minimum distributions (RMDs) are required distributions from qualified retirement plans. RMDs are commonly associated with traditional IRAs, but they also apply to 401(k)s and SEP IRAs. The tax code does not allow taxpayers to keep funds in their qualified retirement plans indefinitely. Eventually, assets must be distributed, and taxes must be paid on those distributions. If a retirement plan owner takes no distributions, or if the distributions are not large enough, he or she may have to pay a 50% penalty on the amount that is not distributed. (Note that distributions are not required to be taken from Roth IRAs while the account owner is alive.)

Generally, RMDs begin in the year that the retirement plan owner attains the age of 72. The first year’s distribution can be delayed to no later than April 1 of the following year. However, delaying the first distribution means taking two distributions in the following year: one for the age-72 year and one for the next year. If an IRA owner dies after reaching age 72 but before April 1st of the next year, no minimum distribution is required because death occurred before the required beginning date. A person who turned 72 in a previous year is required to take the minimum distribution no later than December 31 of each year. The method for determining the minimum amount is explained below.

Even though the tax code mandates minimum distributions after reaching age 72, there is no maximum limit on distributions, and the retirement plan owner can withdraw as much as he or she wishes. However, if more than the required distribution is taken in a particular year, the excess cannot be applied toward the minimum required amounts for future years.

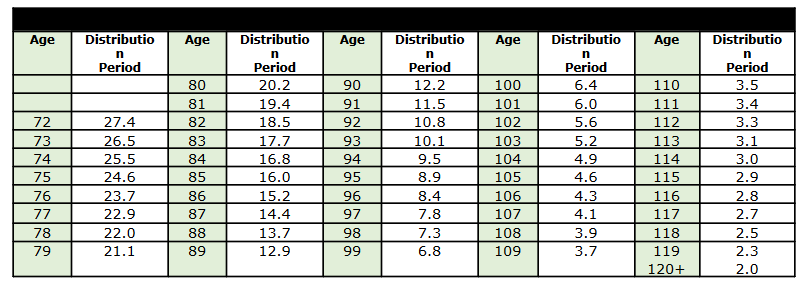

The required withdrawal amount for a given year is equal to the value of the retirement account on December 31 of the prior year divided by the distribution period from a table developed by the IRS. For individual's whose spouse is not the sole designated beneficiary, or, the individual's spouse is the sole designated beneficiary but is not more than 10 years younger than the individual, the Uniform Lifetime Table is used.

Retirement plan owners must calculate the RMD amount for each qualified retirement account separately. However, people who have more than one retirement account of the same type don’t have to take a separate RMD for each. They can aggregate and withdraw the entire amount from just one retirement plan of the same type or withdraw a portion from each plan to satisfy their RMD. So, for example, a distribution from a 401(k) plan won’t satisfy the distribution requirement from an IRA. Similarly, a Roth IRA distribution won’t count toward the RMD for a traditional IRA.

Two tables are not illustrated in this article because of their size: the Joint and Last Survivor Table, which is used to determine RMDs when the sole beneficiary is a spouse who is more than 10 years younger than the plan owner; and the Single Life Table, which is used for certain beneficiary RMD determinations. For table values that are not illustrated above, please call this office.

Example: An IRA account owner is age 75 in this tax year, and the value of his only IRA account was $120,000 on December 31 of last year. His 73-year-old wife is the sole beneficiary of the IRA. From the uniform lifetime table, we determine the owner’s distribution period to be 24.6. Thus, his RMD for the current year is $4,878 ($120,000/24.6). That amount must be withdrawn by no later than December 31 of the current year.

If, in the preceding example, the taxpayer did not withdraw the $4,878, he would be subject to a 50% penalty (additional tax) of $2,439 ($4,878 x 50%). Under certain circumstances, the IRS will waive the penalty if the taxpayer demonstrates reasonable cause and makes the withdrawal soon after discovering the shortfall in the distribution. However, the hassle and extra paperwork involved in asking the IRS to waive the penalty makes avoiding it highly desirable; to do so, always take the correct distribution in a timely manner. Some states also penalize under-distributions.

Even though a qualified plan owner whose total income is less than the return filing threshold is not required to file a tax return, he or she is still subject to the RMD rules and can thus be liable for the under-distribution penalty even if no income tax would have been due on the under-distribution.

BENEFICIARY REQUIRED DISTRIBUTIONS

There are special distribution requirements that apply to beneficiaries which they may be unaware of and that are often misunderstood. Not adhering to the beneficiary distribution requirements can lead to significant complications and penalties.

These beneficiary distributions include special rules for surviving spouse beneficiaries and another set of rules for others. These rules can be complex, and the following is a brief overview. You are cautioned to contact this office to determine how these rules apply to your specific situation. For simplicity, only IRAs are mentioned in the following explanations, but the provisions also apply to qualified retirement plans, such as 401(k)s.

Surviving Spouse – A surviving spouse beneficiary generally has the following options:

1. Treat their deceased spouse’s IRA as their own IRA by designating themself as the account owner.

2. Treat it as their own by rolling it over into their own IRA, or to the extent it is taxable, into a:

a. Qualified employer plan,

b. Qualified employee annuity plan (section 403(a) plan),

c. Tax-sheltered annuity plan (section 403(b) plan),

d. Deferred compensation plan of a state or local government (section 457 plan); or

3. Treat themself as the beneficiary rather than treating the IRA as their own.

Eligible Designated Beneficiaries - These beneficiaries are not subject to the rule (explained below) requiring the account be totally distributed in 10 years (except as noted) and may take lifetime distributions or a lump sum distribution. In addition to a surviving spouse, this category includes:

An individual who is not more than 10 years younger than the account owner (typically a sibling of the decedent but could be someone else).

Disabled or chronically ill individual:

A safe harbor for being considered disabled for this purpose is if the individual is determined to be disabled by the Social Security Administration.

To be eligible the individual must provide to the plan administrator proper documentation of their condition by October 31 of the year following the account owner’s death.

Account Owner’s Minor Child – The IRS has proposed regulations that specify that a minor child is one under the age of 21. Special rules apply to minor children of the account owner (would not apply to a grandchild):

Annual payments, using the single life ables, must be taken until the child reaches age 21.

Once reaching age 21, the child is then subject to the 10-year rule for the balance of the account.

Of course, the beneficiary can always take a lump sum distribution.

Other Beneficiaries – Can take a lump sum distribution or:

Beneficiaries more than 10 years younger than the decedent are subject to the 10-year rule.

Beneficiaries NOT more than 10 years younger than the decedent may take a lifetime payout.

Ten-Year Rule – While it’s true that the account must be depleted by the end of the year that includes the 10th anniversary of the account owner’s death, if the account owner died on or after their required beginning date (RBD), then the beneficiary must ALSO take annual distributions based their life expectancy and then distribute the balance in the 10th year.

PENDING LEGISLATION

There is legislation pending in Congress that would increase the required beginning date for RMDs. A bill in the House of Representatives would change the RBD from the current age 72 to 73 in 2023, 74 in 2030 and 75 in 2033. A Senate bill would change the RBD from 72 to 75, but not until calendar year 2032.

Please contact your tax office for assistance determining your RMD requirements and avoid potential penalties for not complying with those requirements.

How QuickBooks Online Tracks Products and Services

What products and services does your company sell? Do you have enough to fulfill existing and future orders? QuickBooks Online can tell you.

Most small businesses maintain a changing inventory of multiple products. Even if you sell one-of-a-kind goods, you need to know what you’ve sold and what’s available. And if your company sells services, you also have to keep track of what you’re able to offer customers.

QuickBooks Online can meet these needs. It allows you to create detailed records for both products and services. If you carry inventory, it can make sure that you always know what’s available to sell. When you enter sales and purchase transactions, the site draws on the records you’ve created to help you complete invoices, sales receipts, purchase orders, etc., without having to leave the form you’re working on.

Creating your records initially can take some time. And your products and services require regular monitoring and maintenance. But if you’re conscientious about these tasks, you’re not likely to run short on inventory or have too much money tied up in products that aren’t selling fast enough.

Preparing QuickBooks Online

Before you begin creating records and tracking inventory, you need to make sure that QuickBooks Online is set up correctly. Click the gear icon in the upper right. Under Your Company, click Account and settings. Click the Sales tab in the toolbar. You’ll see the Products and services section near the middle of the screen.

Make sure you’ve turned on the Products and services features you’re going to need.

Toggle the slider buttons on and off by clicking on them, and be sure to save your changes when you’re done. One option allows you to turn on price rules. This is still classified as a beta feature, but it’s live on the site. It’s also quite complicated to set up and can create confusion for your customers and revenue loss for you if it’s not done correctly. Let us help if you want to use this tool.

Creating Your Product and Service Records

Your first task, of course, is to build your product and service records. Hover your mouse over Sales in the left vertical toolbar on the home page and select Products and Services. The screen that opens is your home base for dealing with inventory and services. Eventually, it will contain a detailed table containing information about both. Two large buttons at the top of the page warn you when you have Low Stock or you’re Out of Stock.

Click New in the upper right corner. A vertical panel slides out from the right displaying your four options for Product/Service information. They are:

Inventory. If you buy and/or sell products whose quantities you must track, these items are considered inventory.

Non-inventory. You may have products that you buy and/or sell, but you don’t need to track the amount you have in stock. These are considered non-inventory.

Service. These are, well, services that you provide to customers, like landscaping or web design. You might sell these by the hour or project, for example.

Bundle. You might call these assemblies. Bundles are multiple products and/or services that you sell as a package for one price.

Click on Inventory for this example. Here is a partial view of the pane you’ll see:

You can track your inventory levels and reorder points when you create inventory product records in QuickBooks Online.

To create a product or service record, just fill in the blanks on the form and save it. Some fields are optional. In fact, only three are required: Name, Initial quantity on hand, and As of date. Of course, your inventory tracking and the use of product and service records in transactions and reports will be much more effective if you complete as many of the fields as possible. We recommend that you at least provide answers in some additional fields (some of which aren’t shown here), including:

Category (will be useful in reports, for example)

Reorder point (will keep you from running out of items)

Inventory asset account (you can leave the default, Inventory Asset)

Description (for sales forms)

Sales price/rate (what the customer will be charged)

Description (for purchase forms)

Cost (what you pay to buy it)

Expense account (often Cost of Good Sold, but you can ask us to be sure)

If you have other questions that would help you use QuickBooks more effectively, please reach out to your accountant or tax preparer!

Will Your Planned Retirement Income Be Enough after Taxes?

That is an important question because the actual money you have to spend when you retire depends upon the after-tax sources of your retirement income. Thus it is important to understand how the various retirement vehicles are taxed. There is significant diversity in taxation since a retiree must consider both Federal and state taxes on retirement income. Of all the states one might consider retiring to, there are eight that have no state income tax. These are Alaska, Florida, Nevada, South Dakota, Tennessee, Texas, Washington and Wyoming. However, to make up for no revenue from individual income taxes these states may be funded by other types of taxes, such as property taxes, sales taxes, or excise taxes.

Social Security Benefits – Social Security is probably the leading source of retirement for most retirees, and determining the federal taxation can be somewhat complicated and the IRS provides a worksheet. Without using the worksheet we know that no more the 85% of Social Security benefits are subject to federal taxation and in many lower income situations none of the Social Security benefits are taxable.

The actual calculation involves adding your other income to half of your annual Social Security benefit. If the amount is less than $32,000 for married tax filers or less than $25,000 for single filers in 2022, you will avoid federal taxes on your benefits. However, those filing Married Separate will find that 85% of their Social Security benefits are always taxable.

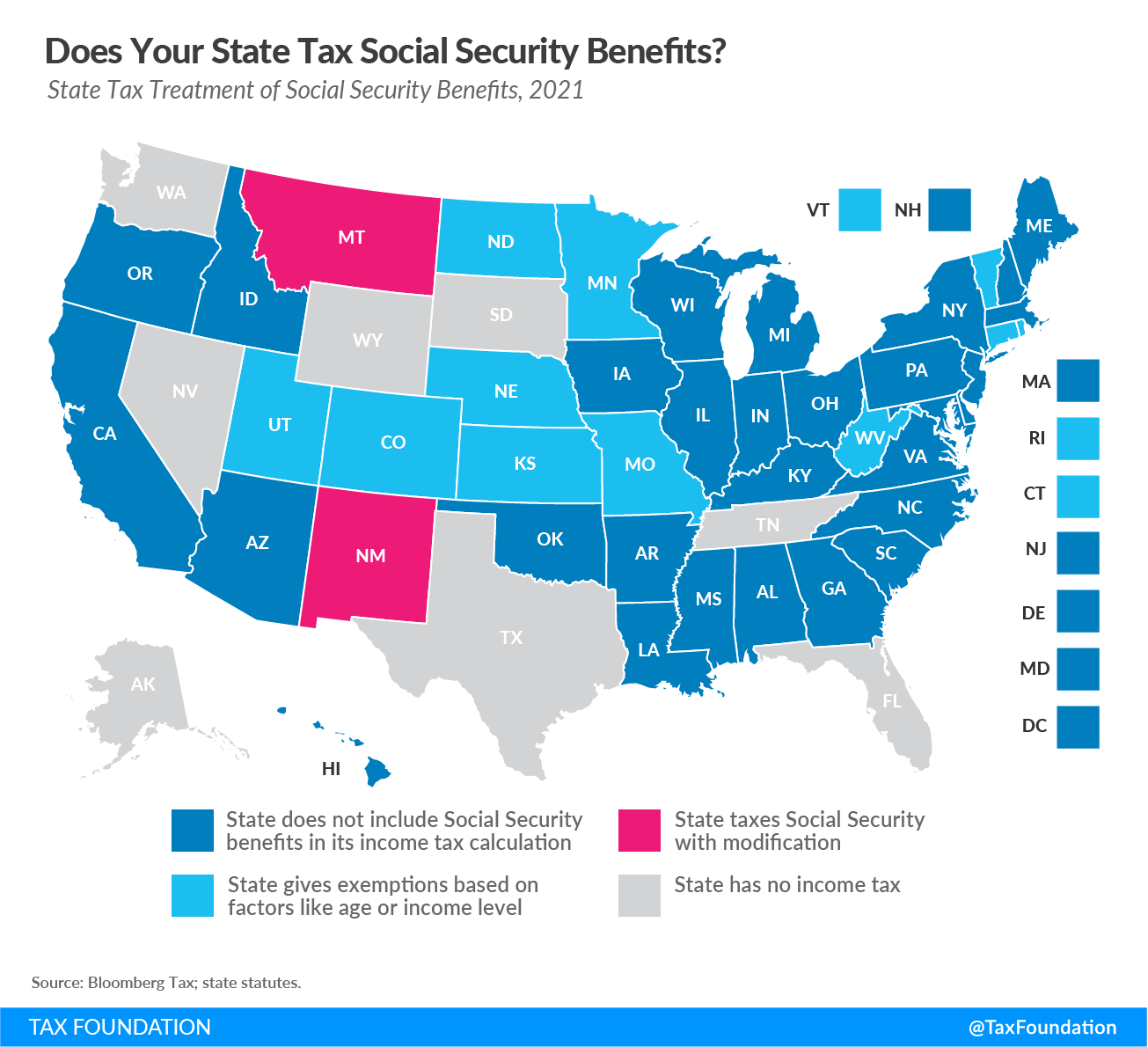

State Tax - Besides the states that have no state tax, there 30 that do not tax Social Security benefits, The balance, VT, CT, RI, WV, MO, MN, ND, NE, KS, CO, UT, NM, and MT, tax Social Security benefits based on factors such as age and income or a modified amount. See the Tax Foundation Map.

{kind=link}

Roth IRA Retirement Account – Roth IRA contributions are limited to the lesser of earned income or the annual limit which is $6,000 ($7,000 if age 50 or over). With a Roth IRA, a taxpayer gets no tax deduction when contributions are made. However, what the taxpayer gets is tax-free accumulation, and after age 59-½, all distributions are tax-free, including the account earnings, provided the 5-year holding period has been met. Since the earnings are also tax free once the age and holding period requirements are satisfied, the sooner an individual begins making contributions, the greater the benefits at retirement. However, contributions to Roth IRA are restricted for higher income taxpayers.

Traditional IRA Retirement Account – Like Roth IRA contributions, traditional IRA contributions are limited to the lesser of earned income or the annual limit which is $6,000 ($7,000 if age 50 or over). Unlike Roth IRAs, generally contributions are deductible in the year of the contribution. Thus future distributions are fully taxable including the earnings. Where an individual also has a qualified retirement plan, the deductibility is phased out for those with higher incomes. However, they can still make non-deductible contributions, in which case a prorated amount of the distributions will be nontaxable. In addition, individuals can elect to make non-deductible contributions which may be appropriate when an individual intends to subsequently convert the traditional IRA to a Roth IRA as discussed next.

Spousal IRA - Generally, IRA contributions are only allowed for taxpayers who have compensation (the term “compensation” includes wages, tips, bonuses, professional fees, commissions, taxable alimony received, and net income from self-employment). Spousal IRAs are the exception to that rule and allow a non-working or low-earning spouse to contribute to his or her own IRA, otherwise known as a spousal IRA, if their spouse has adequate compensation. The maximum amount that a non-working or low-earning spouse can contribute is the same as the limit for a working spouse.

Example: Tony is employed, and his W-2 is $100,000. His wife, Rosa, age 45, has a small income from a part-time job totaling $900. Since her own compensation is less than the contribution limit for the year, she can base her contribution on their combined compensation of $100,900. Thus, Rosa can contribute up to $6,000 to an IRA.

Back-Door Roth IRA - Where a high-income individual would like to contribute to a Roth IRA but cannot because of the high-income limitations, there is a work-around, commonly referred to as a back-door Roth IRA, that will allow funding of a Roth IRA for some individuals. Here is how a back-door Roth IRA works:

First, an individual contributes to a traditional IRA. For higher-income taxpayers who participate in an employer-sponsored retirement plan, a traditional IRA is allowed but is not deductible. Even if all or some portion is deductible, the contribution can be designated as not deductible.

Then, since the law allows an individual to convert a traditional IRA to a Roth IRA without any income limitations, the individual can convert the non-deductible Traditional IRA to a Roth IRA. Since the Traditional IRA was non-deductible, the only tax related to the conversion would be on any appreciation in value of the Traditional IRA before the conversion is completed.

Potential Pitfall – There is a potential pitfall to the back-door Roth IRA that is often overlooked by investment counselors and taxpayers alike that could result in an unexpected taxable event upon conversion. For distribution or conversion purposes, all IRAs (except Roth IRAs) are considered as one account and any distribution or converted amounts are deemed taken ratably from the deductible and non-deductible portions of the traditional IRA, and the portion that comes from the deductible contributions would be taxable.

This may or not may affect the decision to use the back-door Roth IRA method but does need to be considered prior to making the conversion.

Saver’s Credit - Low- and moderate-income workers can take advantage of a special tax credit that helps them save for retirement and earn a special tax credit. This credit helps offset part of the first $2,000 workers voluntarily contribute to traditional or Roth Individual Retirement Arrangements (IRAs), SIMPLE-IRAs, SEPs, 401(k) plans, 403(b) plans for employees of public schools and certain tax-exempt organizations, 457 plans for state or local government employees, and the Thrift Savings Plan for federal employees.

Employer Pensions – Generally, since employer pension plans are fully funded by the employer, pension payments will be fully taxable.

Employee Funded Retirement Plans – These include plans such as 401(k) plans, 403(b) plans, self-employed plans, and SEP IRAs. Since these plans are funded with pre-tax dollars the individual receives a current tax deduction (income deferral); thus, the income and accumulated earnings will be taxable when withdrawn for retirement, after reaching age 59½ or later.

Health Savings Accounts (HSA) - Although the tax code refers to these plans as “health” savings accounts, an HSA can act as more than just a vehicle to pay medical expenses; it can also serve as a retirement account. For some taxpayers who have maxed out their retirement plan options, an HSA provides another resource for retirement savings—one that isn’t limited by income restrictions in the way that IRA contributions are.

Since there is no requirement that the funds be used to pay medical expenses, a taxpayer can pay medical expenses with other funds, allowing the HSA to grow (through account earnings and further tax-deductible contributions) until retirement. In addition, should the need arise, the taxpayer can still take tax-free distributions from the HSA to pay medical expenses. Unlike traditional IRAs, no minimum distributions are required from HSAs at any specific age.

Withdrawals from an HSA that aren’t used for medical expenses are taxable and subject to a 20% penalty, with one exception: an individual age 65 or older will pay income tax on non-medical related distributions from their HSA but won’t owe a penalty for using the funds for other than medical expenses.

Example: Henry, age 70, has an HSA account from which he withdraws $10,000 during the year. He also has unreimbursed medical expenses of $4,000. Of his $10,000 withdrawal, $6,000 ($10,000 – $4,000) is added to Henry’s income for the year, and the other $4,000 is both tax- and penalty-free. If Henry had been 64 years old or younger, he’d be taxed on the $6,000 and pay a penalty of $1,200 (20% of $6,000).

Brokerage Accounts – Some individuals invest in stocks and mutual funds for their future retirement. These investments, if held more than a year, will produce long-term gains or losses. Long-term gains are taxed at zero, 15% or 20% depending on the individual’s total income for the year. However, investments held for less than a year will be taxed as ordinary income (taxed at the individual’s regular tax rate, which could be as high as 37%). In addition, a surtax may apply on the individual’s investment income. It is 3.8% of the lesser of the taxpayer’s net investment income or the excess of their modified adjusted gross income over $250,000 for a joint return or surviving spouse, $125,000 for a married individual filing a separate return, and $200,000 for all others.

Bond Investments – Those who are approaching retirement or have already retired may wish to switch their retirement investments into less uncertain investments since they may not have the longevity to stay the course for a recovery. Bonds provide a safer alternative. Generally, income from municipal bonds is exempt from taxation for federal purposes. In addition, interest earned from municipal bonds issued by an individual’s home state is also exempt from state income taxes.

Home Equity – Provided a retiree has not used up their home equity, that equity can provide a source of retirement income by selling the home and taking advantage of the home gain exclusion of $500,000 for married couples ($250,000 for others). They can do this by downsizing or selling and renting. To qualify for the exclusion the individual must have owned and lived in the home for at least two out of the last five years before the sale. For married taxpayers filing jointly, both spouses must have used the home as their main residence for two of the fives years before the sale, while only one spouse need be the owner for two of the five years.

Reverse Mortgage – As an alternative to selling the home, homeowners aged 62 and older can stay in their home while converting the home equity via a reverse mortgage. With a reverse mortgage the lender pays the homeowner rather than the homeowner making payments. In addition, since the payments constitute home equity they are not taxable.

Whole Life Insurance Cash Value – Cash value accumulated in an insurance policy can also provide a source of income during retirement. The income will be tax-free up to the amount that was paid into the policy.

For some individuals there may be other available sources of retirement income. Please call the office of your tax preparer for assistance in your retirement planning.

Tax and Personal Finance Tips for New Parents

Expanding your family? Whether you’re in the planning stages or your bundle of joy has already arrived, raising a child is one of life’s greatest joys — and biggest expenses. And we’re not just talking about the costs of college. From diapers to daycare, from braces to bicycles, parents are often shocked by the constant outflow of cash that starts days after bringing a new baby home.

While there’s nothing you can do to avoid incurring these expenses, you can definitely soften their impact by educating yourself about what to expect and planning ahead. Below you’ll find a helpful list of mistakes to avoid, resources not to miss, and steps you can take to boost the chances that bringing up a baby will be less of a drain, and more of a pleasure.

Start with a Realistic Budget

Has anybody ever told you that all you need for a baby is a drawer for a bed, a bottle, and a bunch of cloth diapers? There are plenty of people who sing that song, and we have news for you — they’re wrong. If you’ve already given birth then you’re already familiar with some of the bills, but if you’re still in the planning stages, make sure that you include these expenses as you prepare:

Prenatal and postnatal doctor visits for both mom and baby

Baby clothes, nursery furniture, car seats, playpen, glider, highchair, strollers, baby bath, etc.

Childcare

Diapers and wipes, baby medications and ointments, shampoos, etc.

Formula and bottle-feeding supplies or breast pumps and milk-storage bags, or both

And that’s just for the first year or two of parenting. As your child gets older you will need to add on the costs of toys, clothing, bicycles, braces, summer camps, birthday parties …. And if one of the two of you plan to stay home with your child – even part-time – that will significantly impact your disposable household income.

While the government reports that the average cost of raising a child from birth through adulthood is $233,610, those averages include the people who spend the very most, as well as those who spend the very least. To get a realistic sense of how much you can expect to pay, talk to your friends, and ask them to share what they’re spending, especially when it comes to childcare. Those figures can be truly eye-popping.

Take Advantage of Tax Breaks

Plenty of people kid around about their child representing a tax break, but there is truth behind the joke. The government has created several credits and deductions to help alleviate some of the financial burdens of raising a child, but these breaks are not automatic. You have to fill out your tax forms properly and claim the advantages to which you are entitled. Make sure that you are familiar with everything that is available to you. These may include:

Child tax credit – if you have a dependent child and your annual household income falls within the government’s guidelines, you can cut the taxes that you owe significantly

Child and dependent care credit – if you and your partner or spouse file your taxes jointly and pay to have your child cared for by a daycare, nanny, or babysitter, or even to have them attend a summer camp or a before-or-after school program so that you can work or look for work, you can claim a significant portion of these expenses on your income tax.

Earned income tax credit – depending upon income, parents with one or more dependent children may be eligible for the earned income tax credit (EITC), which cuts tax liability

Most Important of All is to Start Thinking Ahead

Perhaps the most essential advice any new parent can be given is to start planning for the future now – and maybe even yesterday. There are plenty of people who spend the early years of their child’s life saying that they don’t know how they’re going to pay for college – and not doing anything about it. The people who start putting small amounts of money away on a regular basis when their kids are small – and who keep doing so throughout their child’s life – are the ones who sleep soundly as college grows nearer. It is never too soon to create a financial plan for your own retirement as well as to address your child’s education, as well as to cushion against an emergency. Your comprehensive financial plan should include:

A retirement fund, whether it’s an employer-sponsored 401(k) or an IRA that you set up for yourself

An emergency fund to help you through anything from a job loss to auto repairs or unexpected medical expenses. Most people suggest having at least three months’ worth of living expenses available, and some say saving enough for six months without an income.

A college fund. Opening a 529 college savings account and making consistent deposits is something you’ll thank yourself for later.

A life insurance policy and a will. It’s nice to run on the assumption that you’ll always be around to support your family. But accidents and unexpected illnesses happen, and far too many people who don’t include life insurance in their economic plans leave behind families that have to deal with their grief and economic situation. It’s also a good idea to take care of basic legal documents like a will, an advance healthcare directive, and power of attorney.

The Basics

If you’re in the planning stages, it’s a very good idea to start saving now, ahead of the costs you’re about to incur for doctor’s bills, hospital fees, and anything not covered by insurance, as well as for income not earned during last weeks of pregnancy/post-partum. You’ll also want to investigate the benefits and family leave policy that your employer offers.

Preparing for a new family member can be overwhelming. For assistance with putting yourself on the right financial path, contact your tax preparer.

To All the Recent College Grads – Some Real-World Financial Advice

Graduating is an enormous accomplishment well worth celebrating, and with the added complication of the global pandemic, your experience was more challenging than most. But now that the last parties are over and you’ve packed up your dorm room or apartment, it’s time to get ready for the next phase of your life: a full-time, professional job. The job market is hot, so finding a position with real potential is highly probable, but it’s important that you know what to do once you start in your new position. We’ve assembled some invaluable advice – both financial and professional — to help you in your journey.

Financial Advice First

You’ve been managing money for yourself for the last few years, but there’s a big difference between working with the money you’ve earned from part-time jobs or internships (or you’ve been gifted from a budget provided by your parents) and knowing how to manage a weekly salary – especially if you’re making a significant amount. You may be tempted to skip returning to your parents’ home, to rent an apartment and buy a car and some work clothes and begin making your way entirely on your own, but that’s not always the smartest thing for you to do financially. Consider the following tips for money management:

As much as you may want to live independently, if you can live with your family long enough to give yourself a bit of savings, you’ll be better off in the long run. It will help you to afford the first and last month’s rents that landlords require, help pay for furniture and other essentials, and let you start paying down any loans that you may have.

Your company will likely offer you a selection of benefits, and the way that you approach these can make a significant difference. If you are offered a 401(k), take advantage of it, and as much as you’d like to hold onto some of your cash, you should always contribute at least as much as your employer is willing to match. Failing to do so is literally giving away free money for your retirement. You should also think carefully about the health insurance that you’re offered. Keep in mind that you are eligible to remain on your parents’ policy until you are 26, so compare the costs and benefits before signing up.

Consider opening a retirement fund that is separate and apart from the 401(k). Retirement may seem like a lifetime away, but getting yourself into the habit of depositing into a Roth IRA is a smart thing to do. The money goes in after-tax and can be taken out when you retire tax-free. You can put away as much as $6,000 per year.

If you’ve been using your parents' credit cards to pay for things and don’t have any loans, then you also don’t have a credit history – and you need one. Take out a credit card in your own name and make sure that you pay them off every month. Take care to pay every bill in full on time.

Learn to keep a budget. Now that you have a predictable salary and take-home pay, it’s time to sit down, write down your total monthly net income and total monthly expenditures on necessities like groceries, rent, utilities, etc., and figure out how much you should be spending, how much you should be saving, how much should go to paying off debts – and stick to it!

Now the Professional Advice

Starting a new job always feels like opening a door to endless possibilities – but that’s especially true of your first job out of college. Though you’re sure to make plenty of mistakes, there are also things that you can set yourself up to do right, right off the bat. Here are some suggestions collected from multiple executives and culled from years of experience:

Don’t be too risk-averse – this is the time to take some chances. As long as your ideas have been thought out, it’s okay to make mistakes – and sometimes your fresh perspective can make a real difference and set you above the crowd.

Let your personal attributes shine. Many people enter the professional world with an idea of how they are supposed to act or who they are supposed to emulate. You were hired for your own characteristics, so be sure to be yourself.

Meet as many people as possible. Networking is an invaluable tool. Each new person that you meet should be considered a link to your future.

Remember that taking your time can be a virtue. Don’t be in such a rush to get where you’re going that you skip steps that can be valuable to your growth.

Take every opportunity to travel. Whether it is throughout the United States or internationally, you will learn a great deal from traveling as part of your job. Not only will you get greater exposure to the way that others do their work or live their lives, but you will be viewed as more open to interesting or diverse assignments.

Don’t turn down responsibilities that are outside of your expertise. The more flexible and adaptive you are, the more you will learn, and the more opportunities that you will be given.

Remember that every job teaches you something. Even a job that you despise has skills that you can carry or use to create a better opportunity. It may not be your dream job, but it may be a necessary step to reaching your dream job.

Be sure to listen carefully to those around you, whether they are your colleagues, your clients, or your supervisors. Being a good listener is highly valued.

As you grow in your career, you may have financial questions or need guidance from someone with more experience. Please contact your firm if you need help navigating personal finance or tax related matters.

Steps You Can Take to Grow Your Business to the Next Level

For small business owners, in particular, growing a business has always been something of a challenge. On the one hand, you don't want to grow too quickly - doing so can significantly damage the trajectory that you've set out on. But at the same time, you also don't want to grow too slowly as this too can cause you to remain stagnant and get passed by some of your competitors.

All of this is also true at higher levels, particularly when it comes to taking that pivotal stop from a $1 million business to a $10 million one. According to studies, most businesses generate about $500,000 in revenue - meaning that they just need to find that next step to get to the desired level. It's certainly not an impossible feat as countless others have done it, but it is something that requires you to keep a few key things in mind.

Growing Your Business: Breaking Things Down

First, it's important to acknowledge that getting to $10 million in revenue for your business isn't actually "the hard part." Most experts agree that getting to that $1 million level is far more difficult.

This ultimately comes down to the disparity between the concepts of "wealth" and "income" - two ideas that people sometimes have a hard time reconciling. Having an overall net wealth of $1 million is certainly an attainable goal. Getting to that point in one year may be less realistic.

Therefore, one needs to understand that ramping up the revenue of a business at the same pace is equally unrealistic. Once you learn to live by the idea of "slow and steady wins the race," you put yourself in a much better position to succeed over the long term.

Indeed, this shift in mindset can pay dividends across the entirety of your organization. You need to re-evaluate your risk aversion, for example, so that you know which opportunities are worth capitalizing on and which must be passed by. You need to be objective with yourself about how tolerant you are to risk in the first place. You should also let that insight inform many of the decisions that follow.

Another way to grow your business from $1 million to $10 million (and beyond) also has to do with being realistic with yourself, albeit in a slightly different way. If your business has grown stagnant, you need to ask yourself why. Is it due to a legitimate lack of opportunity, or is it because of a general pessimism about what the future might hold? The latter is understandable to a certain extent, but it also stands in the way of the growth-minded leader that you need to be. It causes hesitation at moments when action is critical, and it is something that ultimately holds a lot of people back.

Another way to grow your business involves not just learning how to market, but learning how to market correctly. Marketing is a terrific avenue for not only keeping existing customers informed and satisfied but for attracting potential new ones as well. A certain amount of experimentation will be needed and you must spend time getting to learn as much as you can about your audience. Creating buyer personas is a great way to accomplish precisely that.

Finally, you also need to make a determination about what you value in terms of business in general. Some business owners don't actually have an urge to grow - they're perfectly fine existing exactly as they are right now. To be clear, there is absolutely nothing wrong with that. However, if you do have the mindset that growth is in your future, you need to prioritize it in a specific way.

You need to ask yourself WHY you want to grow. Is it for wealth, are you trying to expand, or do you want to leave a legacy behind for the next generation of your family? All of these are important questions to answer because they will dictate a lot of the decisions that you make moving forward.

In the end, growing from a $1 million business to a $10 million one isn't an unattainable goal. It will, however, require you to adjust your mindset and follow crucial best practices like those outlined above.

If you'd like to find out more information about how to grow your business, or if you'd just like to speak to an accounting professional about your own needs in a bit more detail, please contact a professional.

Don’t Overlook Your Charitable Contributions

Your charitable contributions include a wide variety of tax-saving opportunities, some you may not be aware of and some that are frequently overlooked. And there are some contributions that you may believe are deductible that really are not. Being knowledgeable of what is and is not a qualified charity, a qualified charitable contribution, and charitable giving strategies can go a long way towards maximizing your charitable tax deduction.

To be deductible the contributions must be made to qualified charitable organizations, which generally only include U.S. nonprofit groups that are religious, charitable, educational, scientific, or literary in purpose, or that work to prevent cruelty to children or animals. You can ask any organization whether it is a qualified organization, and most will be able to tell you. You can also check by going to IRS.gov/TEOS. This online tool will enable you to search for qualified organizations.

Also, to be able to deduct charitable contributions, one must itemize their deductions. This means that to achieve any tax benefit from your charitable donations, you cannot use the standard deduction, which for example is $12,950 for those filing single, $19,400 filing head of household and $25,900 for married individuals filing jointly for 2022. The standard deduction is adjusted annually for inflation.

If the total of all your itemized deductions does not exceed the standard deduction amount for the year, then you are better off taking the standard deduction, but in doing so, you will get no tax benefit from your charitable contributions. Congress did revise the law to allow limited amounts of cash contributions made in 2020 and 2021 to be deducted without itemizing, but this was only a temporary provision and doesn’t apply in other years.

Bunching – If your charitable deductions are not enough to bring your itemized deductions greater than your standard deduction, the bunching strategy may work for you. When employing the bunching strategy, a taxpayer essentially doubles up on as many deductions as possible in one year, with the goal of itemizing deductions in one year and then taking the standard deduction in the following year. Because charitable contributions are entirely payable at your discretion, they fit right into the bunching strategy.

For example, if you normally tithe at your church, you could make your normal contributions throughout the current year and then prepay the entire subsequent year’s tithing in a lump sum in December of the current year, thereby doubling up on the church contribution in one year and having no charity deduction for church in the next year. Normally, charities are very active with their solicitations during the holiday season, giving you the opportunity to decide whether to make contributions at the end of the current year or simply wait a short time and make them after the end of the year. Be sure you get a receipt or acknowledgment letter from the organization that clearly shows the year when the contribution was made.

As a rule, most taxpayers just wait until tax time to add up their potential deductions and then use the higher of the standard deduction or their itemized deductions. If you want to be more proactive, here are some strategies that might work for you.

Qualified Charitable Distribution – If you are age 70.5 or older, you can make charitable contributions by transferring funds from your IRA account to a charity, which are referred to as qualified charitable distributions (QCDs). The only hitch here is the funds must be transferred directly from the IRA to the charity, meaning your IRA trustee will have to make the distribution to the charity. The tax rules don’t set a minimum amount that needs to be transferred but your IRA trustee may do so. The maximum of all such transfers is $100,000 per year, per taxpayer. Also note that distributions to private foundations and donor-advised funds don’t qualify for the QCD.

Thus, this strategy allows you to make a charitable contribution without itemizing deductions; since these distributions are tax-free, you can’t also claim a deduction for them. Even better, QCDs also count toward your minimum required distribution for the year. Because QCDs are nontaxable, your AGI will be lower, and you can benefit from tax provisions that are pegged to AGI, such as the amount of Social Security income that’s taxable and the cost of Medicare B insurance premiums for higher-income taxpayers.

Caution: Any IRA contributions made after reaching age 70.5 can diminish the tax benefits of this strategy. If any post-age 70.5 IRA contributions have been made, consult with this office before employing this strategy.

If you decide to make a QCD, check with your IRA custodian on the IRA’s rules for how to request the QCD and be sure to give the IRA custodian ample time to complete the process if you are making the request toward the end of the year. Always get a written acknowledgment from the charity, for tax-reporting purposes.

Donor-Advised Funds – Contributing to a donor-advised fund is a way to make a large (and generally deductible) charitable contribution in one year and put funds aside to satisfy the donor’s social obligations to make charitable contributions in future years, without incurring the expenses of setting up a private foundation and satisfying annual filing and other private foundation requirements.

While generally considered a tax strategy for those with an unusually high income for the year, donor-advised funds are available to everyone, although most such funds set up through brokerages have minimum donation requirements, often $5,000–$25,000. Although they may bear the donor's name, donor-advised funds are not separate entities but are mere bookkeeping entries. They are components of a qualified charitable organization. A contribution to a charity's donor-advised fund may be deductible in the year when it is made if it isn't considered earmarked for a particular distributee. The charity must fully own the funds and have ultimate control over their distribution. To document the contribution, the taxpayer must get written acknowledgement from the fund's sponsoring organization that it has exclusive legal control over the contributed assets. Although the donor can advise the charity, which generally will follow the donor’s recommendations, the donor cannot have the power to select distributees or decide the timing or amounts of distributions. The charity must also ensure that all distributions from the fund are arm’s length and do not directly or indirectly benefit the donor.

Example: Don and Shirley donate $25,000 to a donor-advised fund in one year. The $25,000 can be in the form of cash or even appreciated stock. Don and Shirley get a deduction for the full $25,000 as a charitable contribution on their return for the year of the contribution and can suggest the amounts of distributions from the donor-advised fund that should be made to various charities over a number of years. Thus, Don and Shirley achieve a large charitable contribution in one year that can be used to fund their charitable obligations over several years and can claim the $25,000 as an itemized deduction on their return for the year when they made the donation. They do not get a charitable contribution deduction when the funds are paid out from the fund to the various charities.

Volunteer Expenses - If you volunteered your time for a charity or governmental entity, you probably qualify for some tax breaks. Although no tax deduction is allowed for the value of services performed for a qualified charity or federal, state or local governmental agency, some deductions are permitted for out-of-pocket costs incurred while performing the services. The following are some examples:

Away-from-home travel expenses while performing services for a charity, including out-of-pocket round-trip travel costs, taxi fares, and other costs of transportation between the airport or station and hotel, plus 100% of lodging and meals. These expenses are only deductible if there is no significant element of personal pleasure associated with the travel or if your services for a charity do not involve lobbying activities.

The cost of entertaining others on behalf of a charity, such as wining and dining a potential large contributor (but the costs of your own entertainment and meals are not deductible).

If you use your car or other vehicle while performing services for a charitable organization, you may deduct your actual unreimbursed expenses that are directly attributable to the services, such as gas and oil costs, or you may deduct a flat 14 cents per mile for the charitable use of your car. You may also deduct parking fees and tolls.

You can deduct the cost of the uniform you wear when doing volunteer work for the charity, as long as the uniform has no general utility. The cost of cleaning the uniform can also be deducted.

Misconceptions - There are some misconceptions as to what constitutes a charitable deduction, and the following are frequently encountered issues:

No deduction is allowed for contributions of cash or property to the extent the donor received a personal benefit from the donation. Often, the IRS attributes at least some (if not total) personal benefit to amounts spent for items like dinner tickets, church school tuition, YMCA dues, raffles, etc. To determine the allowed contribution amount, subtract the FMV of the “personal benefit” item from the cost and deduct the remainder. Most charities now allocate the deductible, nondeductible portions.

Taxpayers who have purchased tickets for benefit football games, youth-group car washes, parish pancake breakfasts, school plays, etc., with no intention of attending these events, may think they can deduct the expense as a direct contribution to the sponsoring institution. The IRS does not allow such deductions. On the other hand, if the taxpayer returns the ticket to the organization for resale and does not receive a refund of the cost of the ticket, the entire amount paid for the ticket is deductible.

No deduction is allowed for the depreciation of vehicles, computers or other capital assets as a charitable deduction.

Example: Kathy volunteers as a member of the sheriff’s mounted search and rescue team. As part of volunteering, Kathy is required to provide a horse. Kathy is not allowed to deduct the cost of purchasing her horse or to depreciate the value of her horse. She can, however, deduct uniforms, travel, and other out-of-pocket expenses associated with the volunteer work.

However, a taxpayer may deduct the cost of maintaining a personally owned asset to the extent that its use is related to providing services for a charity. Thus, for example, a taxpayer is allowed to deduct the fuel, maintenance, and repair costs (but not depreciation or the fair rental value) of piloting his or her plane in connection with volunteer activities for the Civil Air Patrol. Similarly, a taxpayer—such as Kathy in our example, who participated in a mounted posse that is a civilian reserve unit of the county sheriff’s office—could deduct the cost of maintaining a horse (shoeing and stabling).

A taxpayer who buys an asset and uses it while performing volunteer services for a charity can’t deduct its cost if he or she retains ownership of it. That’s true even if the asset is used exclusively for charitable purposes.

No charitable deduction is allowed for a contribution of $250 or more unless you substantiate the contribution with a written acknowledgment from the charitable organization (including a government agency). To verify your contribution:

Get written documentation from the charity about the nature of your volunteering activity and the need for related expenses to be paid. For example, if you travel out of town as a volunteer, request a letter from the charity explaining why you’re needed at the out-of-town location.

You should submit a statement of expenses to the charity if you are paying out of pocket for substantial amounts, preferably with a copy of the receipts. Then, arrange for the charity to acknowledge the amount of the contribution in writing.

Maintain detailed records of your out-of-pocket expenses—receipts plus a written record of the time, place, amount, and charitable purpose of the expense.

Household Goods and Used Clothing - One of the most common tax-deductible charitable contributions encountered is that of household goods and used clothing. The major complication of this type of contribution is establishing the dollar value of the contribution. According to the tax code, this is the fair market value (FMV), which is defined as the value that a willing buyer would pay a willing seller for the item. FMV is not always easily determined and varies significantly based upon the condition of the item donated. For example, compare the condition of an article of clothing you purchased and only wore once to that of one that has been worn many times. The almost new one certainly will be worth more, but if the hardly worn item had been purchased a few years ago and has become grossly out of style, the more extensively used piece of clothing could be worth more. In either case, the clothing article is still a used item, so its value cannot be anywhere near as high as the original cost. Determining this value is not an exact science. The IRS recognizes this issue and in some cases requires the value to be established by a qualified appraiser.

Remember that when establishing FMV, any value you claim can be challenged in an audit and that the burden of proof is with you (the taxpayer), not with the IRS. For substantial noncash donations, it might be appropriate for you to visit your charity’s local thrift shop or even a consignment store to get an idea of the FMV of used items.

The next big issue is documenting your contribution. Many taxpayers believe that the doorknob hanger left by the charity’s pickup driver is sufficient proof of a donation. Unfortunately, that is not the case, as a United States Tax Court case (Kunkel T.C. Memo 2015-71) pointed out. In that case, the court denied the taxpayer’s charitable contributions, which were based solely upon doorknob hangers left by the drivers who picked up the donated items for the charities. The court stated that “these doorknob hangers are undated; they are not specific to petitioners; they do not describe the property contributed; and they contain none of the other required information.”

Documenting Charitable Contributions – The IRS provides requirements for documenting both cash and non-cash contributions.

Cash Contributions – Taxpayers cannot deduct a cash contribution, regardless of the amount, unless they can document the contribution in one of the following ways:

1. A bank record that shows the name of the qualified organization, the date of the contribution, and the amount of the contribution. Bank records may include:

a. A canceled check,

b. A bank or credit union statement, or

c. A credit card statement.

2. A receipt (or a letter or other written communication) from the qualified organization showing the name of the organization, the date of the contribution, and the amount of the contribution.

3. Payroll deduction records.

Cash Contributions of $250 or More – To claim a deduction for a contribution of $250 or more, the taxpayer must have a written acknowledgment of the contribution from the qualified organization that includes the following details:

The amount of cash contributed;

Whether the qualified organization gave the taxpayer goods or services (other than certain token items and membership benefits) as a result of the contribution, and a description and good faith estimate of the value of any goods or services that were provided (other than intangible religious benefits); and

A statement that the only benefit received was an intangible religious benefit, if that was the case.

If the acknowledgment does not show the date of the contribution, then the taxpayer must have one of the bank records described above that does show the contribution date. If the acknowledgment includes the contribution date and meets the other tests, it is not necessary to also have other records.

The acknowledgment must be in the taxpayer’s hands before the earlier of the date the return for the year the contribution was made is filed, or the due date, including extensions, for filing the return.

Noncash Contributions Deductions of Less Than $250 - A taxpayer claiming a noncash contribution with a value under $250 must keep a receipt from the charitable organization that shows:

1. The name of the charitable organization,

2. The date and location of the charitable contribution, and

3. A reasonably detailed description of the property.

The taxpayer is not required to have a receipt if it is impractical to get one (for example, if the property was left at a charity’s unattended drop site).

Noncash Contributions Deductions of At Least $250 But Not More Than $500 - If a taxpayer claims a deduction of at least $250 but not more than $500 for a noncash charitable contribution, he or she must keep an acknowledgment of the contribution from the qualified organization. If the deduction includes more than one contribution of $250 or more, the taxpayer must have either a separate acknowledgment for each donation or a single acknowledgment that shows the total contribution. The acknowledgment(s) must be written and must include:

1. The name of the charitable organization,

2. The date and location of the charitable contribution,

3. A reasonably detailed description of any property contributed (but not necessarily its value), and

4. Whether the qualified organization gave the taxpayer any goods or services because of the contribution (other than certain token items and membership benefits).

Noncash Contributions Deductions Over $500 But Not Over $5,000 - If a taxpayer claims a deduction over $500 but not over $5,000 for a noncash charitable contribution, he or she must attach a completed Form 8283 to the income tax return and must provide the same acknowledgement and written records that are required for contributions of at least $250 but not more than $500 (as described above). In addition, the records must also include:

How the property was obtained (for example, purchase, gift, bequest, inheritance, or exchange),

The approximate date the property was obtained or—if created, produced, or manufactured by the taxpayer—the approximate date when the property was substantially completed, and

The cost or other basis, and any adjustments to this basis, for property held for less than 12 months and (if available) the cost or other basis for property held for 12 months or more (this requirement, however, does not apply to publicly traded securities).

If the taxpayer has a reasonable case for not being able to provide information on either the date the property was obtained or the cost basis of the property, he or she can attach a statement of explanation to the return.

Deductions Over $5,000 – These donations require time-sensitive appraisals by a “qualified appraiser” in addition to other documentation. When contemplating such a donation, please call this office for further guidance about the documentation and forms that will be needed.

Caution: The value of similar items of property that are donated in the same year must be combined when determining what level of documentation is needed. Similar items of property are items of the same generic category or type, such as coin collections, paintings, books, clothing, jewelry, privately traded stock, land, and buildings. For example, say you donated $5,300 of used furniture to 3 different charitable organizations during the year (a bedroom set valued at $800, a dining set worth $1,000, and living room furniture worth $3,500). Because the value of the donations of similar property (furniture) exceeds $5,000, you would need to obtain an appraisal of the furniture to satisfy the substantiation requirements—even if you donated the furniture to different organizations and at different times during the year. The IRS has strict rules as to who is considered a qualified appraiser.

Do not include items of de minimis value, such as undergarments and socks, in the deductible amount of your contribution, as they specifically are not allowed.

What Do You Do If the IRS Wants to “Audit” Your Tax Return?

The word “audit” tends to strike fear in the hearts of American taxpayers, but the truth is that not every audit is a result of a problem, or that the Internal Revenue Service suspects you of wrongdoing. There are several reasons why the IRS might want to audit your taxes and financial information, and there are several steps that you can take to make the process as painless as possible.

In light of an uptick in identity theft scams involving tax audits and returns, we want to take a moment before delving into this topic to stress that the IRS will never institute an audit process via telephone or email. Taxpayers are always alerted of an upcoming audit by U.S. mail.

Reasons for IRS Audits

Though it is certainly true that some audits are generated by irregularities, the IRS can also request an audit to verify the information contained within your tax papers, to correct a simple mistake such as failing to attach a Schedule, or because the individual taxpayer has some kind of involvement with other taxpayers — such as business partners or investors — whose paperwork raised questions. You may even have been selected for audit as a result of a random selection process designed to gauge taxpayer returns to see how they compare to national norms.

Different types of audits

There are three types of audits conducted by the IRS. In all cases, the taxpayer will be notified of the review by mail.

Correspondence audit – Generally a result of a low-level error or omission, the agency sends out information to the taxpayer referencing the mistake and requesting that revised information be submitted via mail.

Office audit – This type of audit is more intimidating, as it requires the taxpayer to appear at an IRS office, bringing their documentation along with them. These audits are often the result of deductions or credits that are out of the norm, such as an unusually large medical expense deduction for which the agency requires documentation in the form of invoices and payment receipts.

Field audit – The most intrusive of all audits, a field audit involves IRS agents coming to the taxpayer, usually visiting either their place of business or their home in order to review the tax return in detail.

How to prepare for an audit

Receiving notice of a tax audit will put a stutter in the step of even the most meticulous and upstanding taxpayer, but the nerves set off by the notice can easily be offset with the knowledge that you’ve kept good records and maintained copies of all pertinent documents. If you haven’t been keeping careful records, understand that in the face of an audit it will be up to you to prove that you deserve whatever deduction you’ve taken, so amend your ways and start keeping well-organized files of all financial statements, invoices, and receipts. Doing so will not only be a substantial help in case of an audit, but it will also be remarkably helpful should you need to assess your business’ health or put together a financial statement for potential investors or when applying for a loan.

If you are uncomfortable with addressing the IRS questions on your own, you have the right to be represented by a professional of your choice. That might be a CPA, an attorney, or an enrolled agent. This person or persons can go with you or for you to any face-to-face meetings. There is no requirement that you attend an audit session unless the IRS specifically requests your presence.

After the audit is over, you will be provided with a report. If you agree with the contents of the report, you can simply sign it or whatever assenting form the auditor provides to you.

The taxpayer bill of rights

You may think yourself at the mercy of the IRS, but Congress enacted a taxpayer bill of rights that specifically outlines the IRS’ tax collecting abilities as well as the protections offered to taxpayers in the face of IRS collections. The taxpayer bill of rights includes:

Right to be Informed

Right to Quality Service

Right to pay no more than the Correct Amount of Tax

Right to Challenge the IRS’s position and be Heard

Right to Appeal an IRS’s decision in an Independent Forum

Right to Finality

Right to Privacy

Right to Confidentiality

Right to Retain Representation

Right to a Fair and Just system

What if you don’t agree with the audit decision?

Knowing that you have rights is nice, but pushing back against the decision of an IRS examiner can feel challenging. If you’ve complied with all of the examiner’s requests and now find yourself with a Revenue Agent Report that you disagree with, there are specific steps that you can take. You can:

Ask for an informal conference with the examiner’s manager before the deadline provided within the report.

Ask for an Appeals conference to occur before the deadline provided within the report.

If you have received a Statutory Notice of Deficiency, you can also file a petition with the tax court.

How to Get Through an Audit

There is no shame in being unnerved by an IRS audit, but there are several ways that you can minimize the stress that you feel.

Don’t hesitate to request a postponement if you need time to get your documents together.

Familiarize yourself with your rights

Be honest

Discuss your audit strategies with your Authorized Representative, whether that is your CPA, attorney, or another person. That person will respond directly to the assigned IRS agent.

Don’t try to fake your way through an audit. Have the information that is requested so that you can get through it more quickly.

Don’t hesitate about reaching out to the auditor if you disagree with the examination report that they have produced.

Remember that if you are unable to pay a tax liability or disagree with the auditor’s assessment, negotiation is a possibility.

One of the most important decisions you can make in the face of an audit letter is to work with an experienced tax representative who can help you with both your preparations and your response. For information on the assistance your tax preparer can provide, contact their office today.